All Categories

Featured

Table of Contents

When you make rate of interest in an annuity, you commonly don't need to report those revenues and pay revenue tax obligation on the earnings every year. Development in your annuity is protected from individual earnings tax obligations.

While this is an introduction of annuity taxes, get in touch with a tax specialist prior to you make any type of choices. Annuity fees. When you have an annuity, there are a number of information that can affect the tax of withdrawals and earnings settlements you receive. If you put pre-tax money right into a specific retired life account (IRA) or 401(k), you pay tax obligations on withdrawals, and this holds true if you fund an annuity with pre-tax money

If you contend least $10,000 of earnings in your annuity, the entire $10,000 is dealt with as revenue, and would generally be strained as common revenue. After you wear down the incomes in your account, you receive a tax-free return of your original round figure. If you convert your funds into a guaranteed stream of revenue settlements by annuitizing, those repayments are split right into taxable parts and tax-free sections.

Each payment returns a part of the cash that has currently been tired and a section of passion, which is taxable. For instance, if you obtain $1,000 monthly, $800 of each repayment could be tax-free, while the continuing to be $200 is taxed earnings. Ultimately, if you outlast your statistically established life expectations, the whole amount of each settlement might come to be taxable.

Considering that the annuity would have been moneyed with after-tax money, you would certainly not owe tax obligations on this when taken out. Since it is categorized as a Roth, you can also possibly make tax-free withdrawals of the growth from your account. To do so, you must adhere to numerous internal revenue service regulations. As a whole, you have to wait up until at least age 59 1/2 to take out earnings from your account, and your Roth must be open for at the very least five years.

Still, the other functions of an annuity might outweigh earnings tax treatment. Annuities can be devices for deferring and managing taxes.

Tax on Annuity Income Riders death benefits for beneficiaries

If there are any kind of penalties for underreporting the earnings, you could be able to ask for a waiver of charges, but the passion normally can not be forgoed. You may be able to prepare a payment plan with the internal revenue service (Annuity beneficiary). As Critter-3 stated, a local specialist could be able to assist with this, but that would likely cause a little extra expenditure

The initial annuity contract owner have to include a survivor benefit stipulation and call a recipient - Guaranteed annuities. There are various tax consequences for partners vs non-spouse beneficiaries. Any type of beneficiary can choose to take an one-time lump-sum payment, nevertheless, this comes with a hefty tax concern. Annuity beneficiaries are not restricted to people.

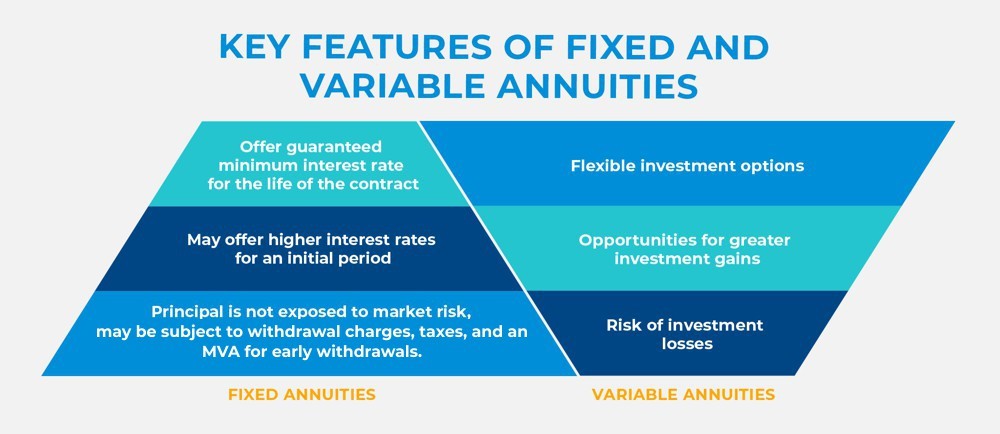

Fixed-Period Annuity A fixed-period, or period-certain, annuity makes sure payments to you for a specific length of time. For instance, repayments might last 10, 15 or twenty years. If you die throughout this time around, your selected beneficiary receives any type of continuing to be payouts. Life Annuity As the name suggests, a life annuity guarantees you payments for the rest of your life.

Multi-year Guaranteed Annuities beneficiary tax rules

If your contract consists of a survivor benefit, staying annuity repayments are paid out to your recipient in either a round figure or a series of repayments. You can select a single person to get all the readily available funds or several individuals to receive a percentage of staying funds. You can also choose a nonprofit company as your beneficiary, or a trust established as component of your estate plan.

Doing so enables you to maintain the very same options as the original owner, including the annuity's tax-deferred status. You will also be able to obtain staying funds as a stream of settlements as opposed to a lump amount. Non-spouses can likewise acquire annuity settlements. They can not alter the terms of the contract and will only have access to the designated funds detailed in the initial annuity agreement.

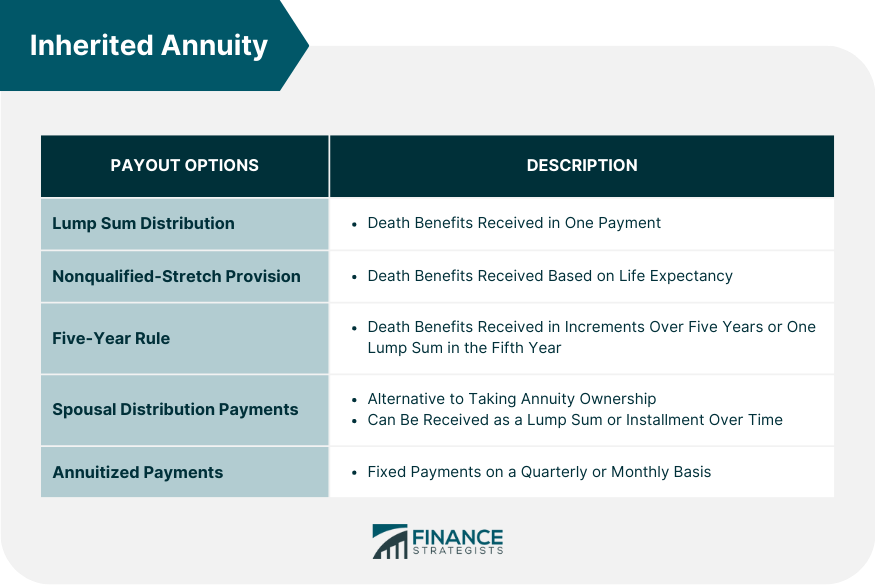

There are 3 major methods recipients can get inherited annuity repayments. Lump-Sum Circulation A lump-sum circulation permits the recipient to obtain the contract's whole staying worth as a single payment. Nonqualified-Stretch Arrangement This annuity agreement provision allows a beneficiary to receive settlements for the rest of his or her life.

Any recipient consisting of spouses can choose to take an one-time round figure payout. In this situation, tax obligations are owed on the whole difference in between what the original owner spent for the annuity and the survivor benefit. The lump amount is tired at regular revenue tax obligation prices. Lump sum payouts bring the highest possible tax obligation concern.

Spreading payments out over a longer period is one way to prevent a large tax bite. If you make withdrawals over a five-year duration, you will certainly owe taxes only on the raised value of the section that is withdrawn in that year. It is additionally less most likely to press you right into a much higher tax bracket.

Inherited Guaranteed Annuities tax liability

This offers the least tax obligation exposure but also takes the longest time to receive all the cash. Structured annuities. If you have actually acquired an annuity, you typically must choose concerning your survivor benefit quickly. Decisions regarding how you wish to get the cash are frequently final and can not be changed later

An inherited annuity is a financial product that enables the beneficiary of an annuity agreement to continue receiving settlements after the annuitant's death. Inherited annuities are frequently utilized to supply earnings for loved ones after the death of the main breadwinner in a family. There are two sorts of acquired annuities: Immediate inherited annuities begin paying right now.

Tax implications of inheriting a Structured Annuities

Deferred acquired annuities permit the recipient to wait up until a later date to start obtaining repayments. The most effective thing to do with an inherited annuity relies on your economic circumstance and requirements. An immediate inherited annuity might be the most effective option if you require immediate revenue. On the various other hand, if you can wait a while prior to starting to obtain payments, a deferred inherited annuity might be a far better selection. Annuity interest rates.

It is essential to speak to a monetary advisor prior to making any kind of choices concerning an acquired annuity, as they can help you establish what is finest for your specific circumstances. There are a couple of dangers to think about before investing in an acquired annuity. Initially, you need to recognize that the federal government does not assure acquired annuities like other retired life items.

Do beneficiaries pay taxes on inherited Annuity Withdrawal Options

Second, acquired annuities are usually complicated financial products, making them hard to recognize. Speaking to a financial consultant prior to spending in an acquired annuity is vital to ensure you completely understand the threats entailed. There is constantly the threat that the worth of the annuity could go down, which would certainly decrease the quantity of cash you get in settlements.

{kind=link}

Table of Contents

Latest Posts

Decoding Annuities Fixed Vs Variable A Comprehensive Guide to Investment Choices Breaking Down the Basics of Fixed Vs Variable Annuity Pros Cons Features of Annuities Variable Vs Fixed Why Variable An

Breaking Down Your Investment Choices Everything You Need to Know About Financial Strategies What Is Fixed Interest Annuity Vs Variable Investment Annuity? Features of Fixed Vs Variable Annuity Why De

Decoding How Investment Plans Work A Comprehensive Guide to Immediate Fixed Annuity Vs Variable Annuity Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Choosing t

More

Latest Posts